Start now: max out retirement accounts, cut debt, and boost savings each year.

I have spent years helping people plan money for later. I know the common gaps and the fixes that work. This guide shows clear steps on how to save for retirement in your 40s. You will get practical rules, simple math, and real examples you can use today.

Why your 40s matter and what you can still achieve

Your 40s are a powerful decade for retirement saving. You still have 20 or more years to grow money. That time lets compound interest do a lot of work if you act now.

Many people delay and then panic. That creates poor choices and stress. With focus, you can close much of the shortfall. I will show savings targets, account choices, and real moves that helped clients recover lost time.

Quick assessment: know where you stand

Start with simple numbers. Write down current savings, monthly retirement contributions, expected Social Security, and debts. Estimate your desired retirement income as a percent of your current income.

Use a short rule of thumb:

- Aim for 25 times your expected annual retirement spending saved by retirement.

- If you earn $80,000 now and want 70% of that, aim for $1.4 million (80,000 × 0.7 × 25).

Run the math and note the gap. This gap shows how much you must save each year. That clarity makes the next steps easier.

How to save for retirement in your 40s: a step-by-step plan

This is a simple plan you can start today. Follow each step and track progress every quarter.

- Raise your savings rate now.

- Increase contributions by 1% every month until you reach 15–25% of pay.

- Max out tax-advantaged accounts.

- Prioritize 401(k), 403(b), and IRAs. Use catch-up contributions when eligible.

- Pay down high-cost debt fast.

- Target credit cards and high-rate loans before low-rate mortgage debt.

- Build a safe cash buffer.

- Keep 3–6 months of expenses in an easy-to-access account.

- Add taxable investing for flexibility.

- Use low-cost index funds or ETFs for extra savings beyond retirement accounts.

- Boost income with side work.

- Freelance, teach, or sell a skill. Use extra income to fuel retirement contributions.

- Revisit your plan yearly.

- Rebalance, raise savings, and tweak goals every year.

I used this plan when I was 42. I raised my 401(k) contributions and did a small freelance side job. That added 10% more to savings each year and made a big difference by age 50.

Tax-advantaged accounts and catch-up rules

Pick accounts that cut taxes and grow money faster. Know limits and catch-up rules.

- 401(k) and 403(b) accounts

- Contribute pre-tax or use a Roth option. Employer match is free money. Catch-up after 50 lets you add more.

- Traditional and Roth IRAs

- IRAs offer more control. Roth IRAs grow tax-free if rules are met. Income limits may apply.

- Health savings accounts (HSA)

- HSA offers triple tax benefits if you qualify. Use for medical costs now or as an extra retirement account.

If you are in your 40s, max what you can now. Every extra dollar saved compounds for two decades or more. That is huge.

Investment strategy for people in their 40s

You need growth but also some safety. Your portfolio should match your timeline and risk comfort.

- Allocate for growth and balance

- A common split is 70% stocks and 30% bonds in your 40s. Adjust up or down by comfort.

- Use low-cost index funds

- Keep fees low to boost long-term returns. High fees erode gains.

- Rebalance yearly

- Rebalancing keeps risk in check. It locks in gains and restores target mix.

- Consider target-date funds

- These simplify choices. Pick one that matches your retirement year.

I once advised a client to reduce fee funds and switch to low-cost ETFs. The client kept the same risk level but saved thousands in fees over a decade.

Reduce spending and free up cash

Small changes add up quickly. Free cash is the fast path to higher retirement savings.

- Cut recurring costs

- Review subscriptions, insurance, and phone plans. Cancel unused services.

- Trim big expenses

- Refinance a mortgage if rates drop. Drive a reliable used car longer.

- Prioritize savings in your budget

- Pay yourself first by automating contributions. Treat savings like a bill.

I trimmed a few recurring services and redirected that money to retirement. Over time it became a meaningful annual boost.

Increase income with practical moves

Higher income makes saving easier. Use skills and time wisely.

- Ask for raises with evidence

- Document wins and ask your manager. Small raises compound.

- Start a side gig

- Teach online, consult, or pick a local gig. Put all extra pay straight to retirement.

- Monetize hobbies

- Turn a hobby into small income. Use it to top up accounts.

When I freelanced weekends for a year, I put earnings into a taxable account and then into retirement later. That habit helped me catch up faster.

Social Security and retirement age choices

Understand Social Security basics. Your choice of claiming age changes your benefit.

- Claiming early reduces monthly benefits.

- Claiming later increases the monthly check up to age 70.

- Combine Social Security with personal savings in your plan.

Plan a claiming strategy that matches your health, work plans, and cash needs. Include expected benefits in your gap math.

Common mistakes to avoid

Avoid these traps that slow progress and waste money.

- Relying only on Social Security

- Social Security is a base, not a full plan. Save more than that.

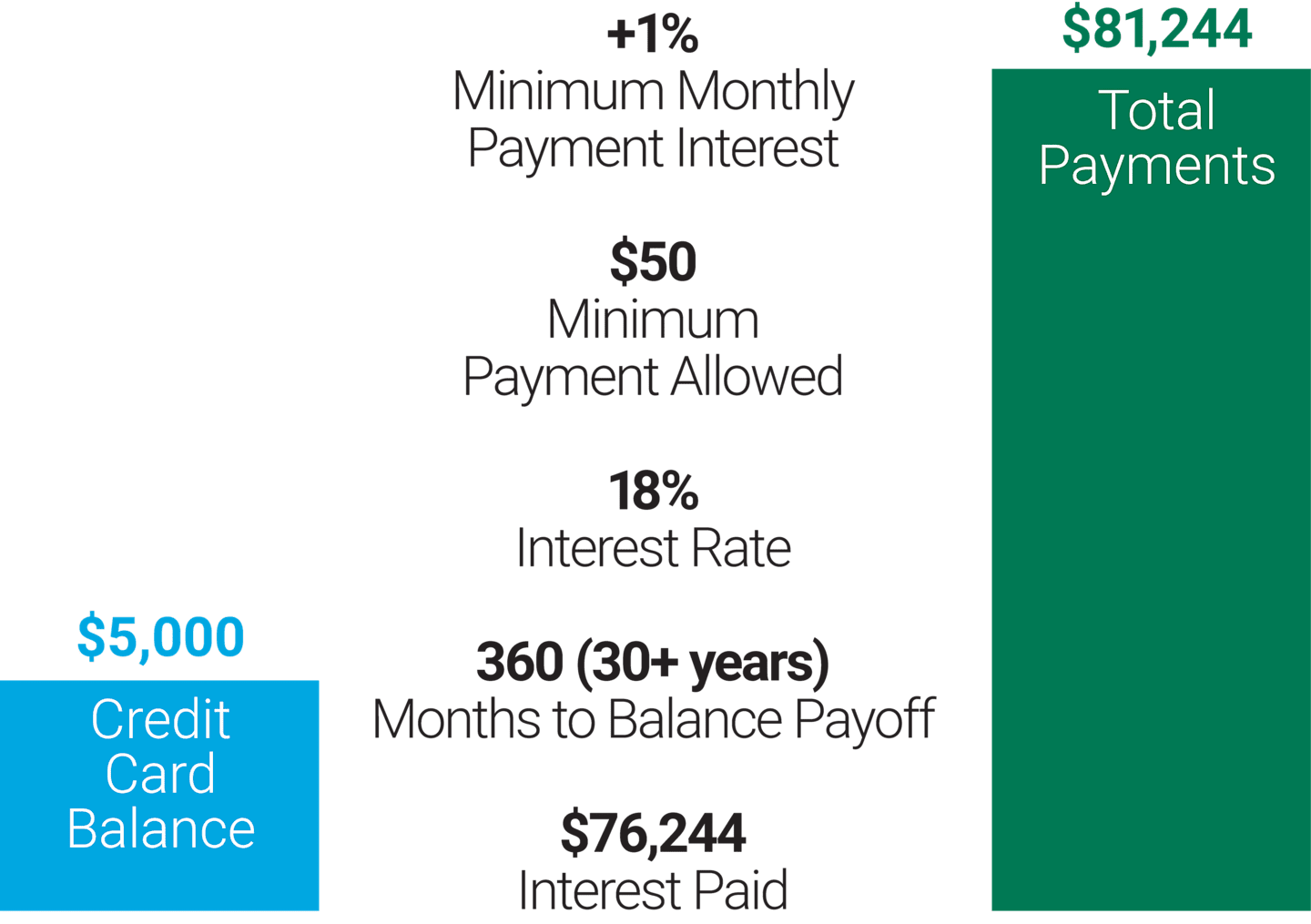

- Paying high fund fees

- Fees eat returns. Choose low-cost funds.

- Ignoring employer match

- Not taking full match is leaving money on the table.

- Draining retirement accounts early

- Try to keep retirement money for retirement. Early withdrawals cost penalties and income tax.

I once saw a couple cash out a retirement plan for a home. They lost growth and paid taxes. They later had to save more to fill the gap.

How to save for retirement in your 40s: simple savings examples

Short examples make the math real. These numbers assume steady returns and simple compounding.

Example 1: 10 years to save more

- Age 45 with $150,000 saved. Save $20,000 per year. 6% return. Result by 65 ≈ $1.1M.

Example 2: steady increase

- Age 40 with $100,000 saved. Save 15% of $80,000 salary. Raise savings rate by 1% per year. Result by 65 can reach $1M+.

Numbers vary by return and time. But the pattern holds: higher savings and time matter.

Tracking progress and staying motivated

Simple tracking keeps momentum. Check numbers often but stress less.

- Quarterly reviews

- Look at account balances and adjust contributions.

- Use simple dashboards

- Many brokerages offer easy views of progress.

- Celebrate milestones

- Reaching each 25% of your target is worth a small reward.

I set short goals and a small celebration for each. It made saving less dull and more steady.

Frequently Asked Questions of how to save for retirement in your 40s

Can I still retire if I start saving aggressively in my 40s?

Yes. Starting aggressively in your 40s can build a solid nest egg. With consistent high savings and smart investing, many people reach comfortable retirements.

How much should I save each year in my 40s?

Aim for 15–25% of your gross income, including employer match. Increase the rate each year to close any gap.

Should I pay off debt or save for retirement first?

Prioritize high-interest debt first, then balance debt payoff with retirement saving. Keep some emergency savings while paying down debt.

Are Roth accounts good for people in their 40s?

Yes. Roth accounts give tax-free growth and tax-free withdrawals later. They can be especially valuable if you expect higher taxes in retirement.

What is a realistic savings goal by age 50?

A common goal is 6–8 times your pre-retirement income by 50. Adjust this for your retirement age, lifestyle, and other income sources.

How do catch-up contributions work?

At age 50 you can add extra money to 401(k)s and IRAs beyond standard limits. These boosts help close gaps faster.

Should I change my investment mix in my 40s?

You may shift slightly toward a balanced mix to reduce volatility but keep growth. Review risk and rebalance yearly.

Conclusion

Your 40s are a chance to act with clarity and purpose. Start with a clear gap analysis. Raise contributions, use tax-advantaged accounts, cut fees, and add income where you can. Small, steady changes now can lead to big results later. Take one step today: increase your retirement contribution by 1% this month and schedule a review in three months. Share your progress, ask questions, or subscribe for more guides on saving and investing.

Retirement Planning Writer & Financial Lifestyle Expert

Michael Reynolds is a senior contributor at RetirementGazette.com, where he focuses on helping readers navigate the journey toward a secure and fulfilling retirement. With over a decade of experience in personal finance, retirement planning, and lifestyle writing, Michael combines practical strategies with easy-to-understand guidance tailored for both pre-retirees and those already enjoying their golden years.

His work covers a wide range of topics including retirement income strategies, smart investing, post-retirement careers, and everyday financial decisions that shape long-term stability. Michael believes that retirement is not just about saving money—it’s about creating a balanced life with purpose, flexibility, and peace of mind. This perspective aligns with modern retirement thinking, where financial planning and lifestyle choices go hand in hand.

At RetirementGazette.com, Michael is committed to delivering well-researched, unbiased, and actionable content. He carefully analyzes financial trends, expert insights, and real-world scenarios to help readers make confident decisions about their future. His mission is simple: to empower individuals with the knowledge they need to retire smarter, live better, and enjoy every stage of life after work.