How long will retirement savings last depends largely on withdrawal rate and market returns — typically 15–30 years.

I’ve spent years modeling retirements for clients and running numbers across markets and lifespans. In this article I’ll show you how long will retirement savings last, step by step. You’ll learn clear methods, real examples, and practical moves to extend your money in retirement.

Why how long will retirement savings last matters

Knowing how long will retirement savings last shapes every retirement decision. It guides choices about work, Social Security timing, risk, and health care planning. If you underestimate duration, you may run out of money. If you overestimate, you might underspend and miss life goals.

Key factors that determine how long will retirement savings last

Several core drivers change the answer for each person. These are easy to understand but powerful in effect.

- Withdrawal rate. The percent of savings you use in year one, often adjusted for inflation. Higher rates shorten longevity.

- Investment returns. Market gains and losses change the balance over time. Volatility matters, especially early.

- Inflation. Rising prices erode purchasing power and shorten how long savings buy the same lifestyle.

- Life expectancy. Living longer raises the time your money must cover. Expect variability.

- Expenses and lifestyle. Housing, health care, and travel choices shift the math quickly.

- Guaranteed income. Pensions or annuities reduce reliance on savings and extend other assets.

I use simple scenarios in my work to show clients the effect of each factor. When people change one or two variables, the result can swing by a decade or more.

How to estimate how long will retirement savings last

Start with a straightforward calculation. Then refine with more advanced tools.

- Step 1. Take your total retirement savings and add guaranteed income like pensions.

- Step 2. Decide a withdrawal strategy. A common rule is the 4% rule: withdraw 4% of savings in year one, then adjust for inflation.

- Step 3. Estimate returns and inflation. Use conservative long-term return assumptions if you want safety.

- Step 4. Run the numbers. See how long funds last under different scenarios.

Example: If you have $1,000,000 and follow a 4% rule, you start with $40,000 a year. With moderate returns and 2% inflation, that portfolio historically lasted 25–30 years in many simulations. If you start at 5% withdrawals, that timeline shrinks notably.

Two more approaches to refine estimates:

- Monte Carlo simulations. These run many market scenarios to estimate the probability your savings last 20, 30, or 40 years.

- Bucketing or glidepath models. These combine short-term cash reserves with long-term growth assets to reduce sequence-of-returns risk.

Using these tools, you can answer how long will retirement savings last with probabilities rather than a single fixed number.

Strategies to extend how long will retirement savings last

You can influence the timeline with practical moves. I’ve helped clients use many of these tactics.

- Lower initial withdrawal rate. Even a 0.5%–1% cut can add years to your horizon.

- Delay Social Security. Waiting increases guaranteed income and reduces pressure on savings.

- Shift asset allocation gradually. More equity early can boost returns; add bonds later to reduce volatility.

- Work part-time in early retirement. Earned income reduces withdrawals and delays tapping principal.

- Reduce discretionary spending. Small cuts on travel or subscriptions compound over decades.

- Use annuities selectively. A longevity annuity or lifetime payout can cover late-life costs.

- Optimize taxes. Roth conversions, tax-efficient withdrawals, and municipal bonds can improve net income.

I once advised a couple to delay full retirement by two years and trim one major expense. Those two choices together stretched their portfolio by roughly five years in our model.

Real-life examples and a personal perspective on how long will retirement savings last

Concrete examples help make this real. Here are three short case studies I’ve worked on.

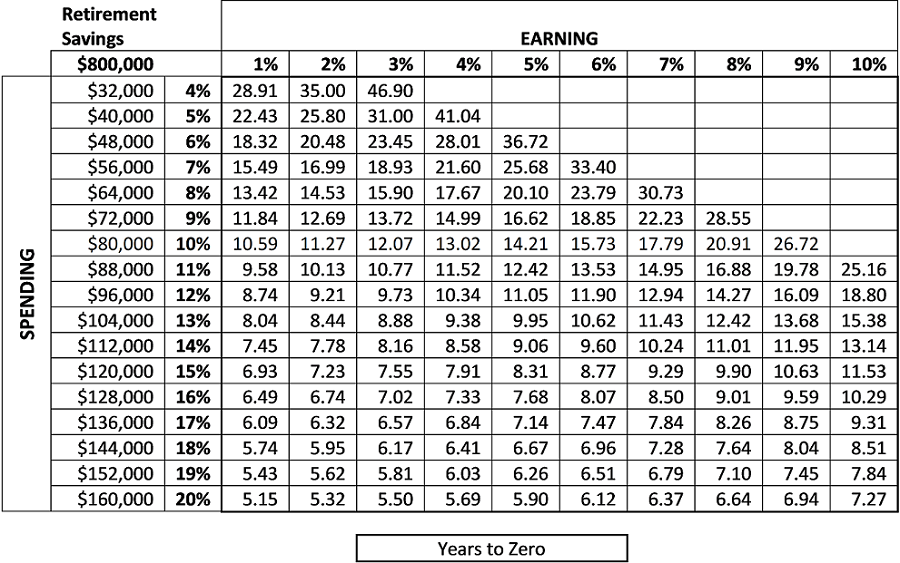

- The conservative couple. Age 65, $800,000 savings, no pension. They chose a 3.25% starting withdrawal and kept a 60/40 portfolio. Their plan showed a high chance of lasting 30+ years.

- The ambitious spender. Age 62, $1.2M, wants $80k per year. They used a 5% withdrawal and a high-equity portfolio. Simulations showed a significant risk of running out before age 90.

- My own learning. Early in my career I advised a client to accept a 4.5% withdrawal rate. Markets then performed poorly for several years. We adjusted spending and delayed a major purchase. That experience taught me to plan buffers and conservative entry withdrawals.

Lessons learned:

- Small behavior changes can drive big outcomes.

- Sequence of returns is crucial in early retirement years.

- Flexibility in spending is a powerful tool.

Common mistakes and limitations when estimating how long will retirement savings last

Mistakes can make the difference between stability and shortfall. Watch for these.

- Using optimistic return assumptions. Markets vary and past returns don’t guarantee future results.

- Ignoring sequence-of-returns risk. Early losses paired with large withdrawals are dangerous.

- Forgetting health care and long-term care costs. These can be large and unpredictable.

- Treating the estimate as fixed. Life changes—health, family needs, and markets—require plan updates.

- Overreliance on a single rule. The 4% rule helps, but it is not one-size-fits-all.

Be transparent about uncertainty. Good plans include guardrails and contingency options.

Tools and resources to calculate how long will retirement savings last

Several practical tools help do the math. Use them to test scenarios and stress-test plans.

- Retirement calculators. Use ones that allow custom withdrawal rates, tax settings, and inflation assumptions.

- Monte Carlo tools. Look for simulations that show success probabilities across many market runs.

- Spreadsheet models. A simple spreadsheet can model withdrawals, returns, and inflation year by year.

- Financial advisors. A fiduciary advisor can add personalized planning and tax-aware strategies.

- Professional software. Planners use software that models cash flow, Social Security, and long-term care.

I often start clients on a spreadsheet before moving to advanced simulations. That helps them understand the mechanics and see how each assumption matters.

Frequently Asked Questions of how long will retirement savings last

How does the 4% rule relate to how long will retirement savings last?

The 4% rule is a simple guideline that aims to make savings last about 30 years. It is a starting point, but personal factors and market conditions can change the outcome.

Will my retirement savings last longer if I invest more aggressively?

More equity exposure can increase expected returns and potentially extend savings, but it raises volatility and sequence-of-returns risk. A balanced plan usually mixes growth with protection.

Does delaying Social Security affect how long will retirement savings last?

Yes. Delaying Social Security increases guaranteed income and reduces withdrawals from savings, which can extend portfolio longevity. Even a small delay often improves the odds of not running out.

How should I adjust withdrawals if markets fall early in retirement?

Reduce discretionary spending, postpone large purchases, or draw more from cash reserves while markets recover. Small adjustments early can preserve long-term sustainability.

Can annuities help determine how long will retirement savings last?

Annuities convert part of your savings into guaranteed lifetime income, which lowers the burden on the rest of your portfolio. They can be a useful tool to secure longevity coverage.

Conclusion

Knowing how long will retirement savings last is not about a single number. It’s about testing scenarios, choosing sensible withdrawal strategies, and building flexibility. Use conservative assumptions, plan for surprises, and update your plan regularly.

Take action today: run a simple calculation, try a Monte Carlo or spreadsheet model, and talk to a trusted advisor if needed. If this article helped, subscribe for updates or leave a comment with your situation and I’ll suggest next steps.

Retirement Planning Writer & Financial Lifestyle Expert

Michael Reynolds is a senior contributor at RetirementGazette.com, where he focuses on helping readers navigate the journey toward a secure and fulfilling retirement. With over a decade of experience in personal finance, retirement planning, and lifestyle writing, Michael combines practical strategies with easy-to-understand guidance tailored for both pre-retirees and those already enjoying their golden years.

His work covers a wide range of topics including retirement income strategies, smart investing, post-retirement careers, and everyday financial decisions that shape long-term stability. Michael believes that retirement is not just about saving money—it’s about creating a balanced life with purpose, flexibility, and peace of mind. This perspective aligns with modern retirement thinking, where financial planning and lifestyle choices go hand in hand.

At RetirementGazette.com, Michael is committed to delivering well-researched, unbiased, and actionable content. He carefully analyzes financial trends, expert insights, and real-world scenarios to help readers make confident decisions about their future. His mission is simple: to empower individuals with the knowledge they need to retire smarter, live better, and enjoy every stage of life after work.