Most public teachers need about 20–30 years of service for a full pension; age rules vary.

If you’re thinking of a career in education—or already teaching—you may be wondering: how many years to retire as a teacher?

The answer depends on your location, pension system, and when you started teaching. However, there are common patterns that can help you estimate your retirement timeline.

I’ve worked with teachers and school retirement systems for years, helping educators answer the core question of how many years to retire as a teacher. This article explains the rules, shows real calculations, compares systems, and offers practical strategies so you can plan retirement with confidence. Read on to learn the exact steps and options that apply to your situation, and get clear examples you can use today.

Understanding how many years to retire as a teacher

Retirement eligibility for teachers depends on service years, age, and the pension system. Many public pension plans use combinations like fixed-service thresholds (for example, 25 or 30 years) or age-plus-service “rules” (for example, age 55 with 10 years, or the Rule of 80). Private school teachers and adjuncts often rely on Social Security or personal savings instead.

Pension plans differ in benefit formulas and early-retirement penalties. Common structures include a final average salary multiplied by years of service and a multiplier. Knowing your plan’s specifics makes answering how many years to retire as a teacher simple and actionable.

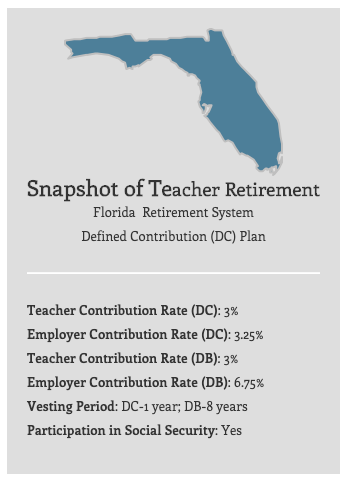

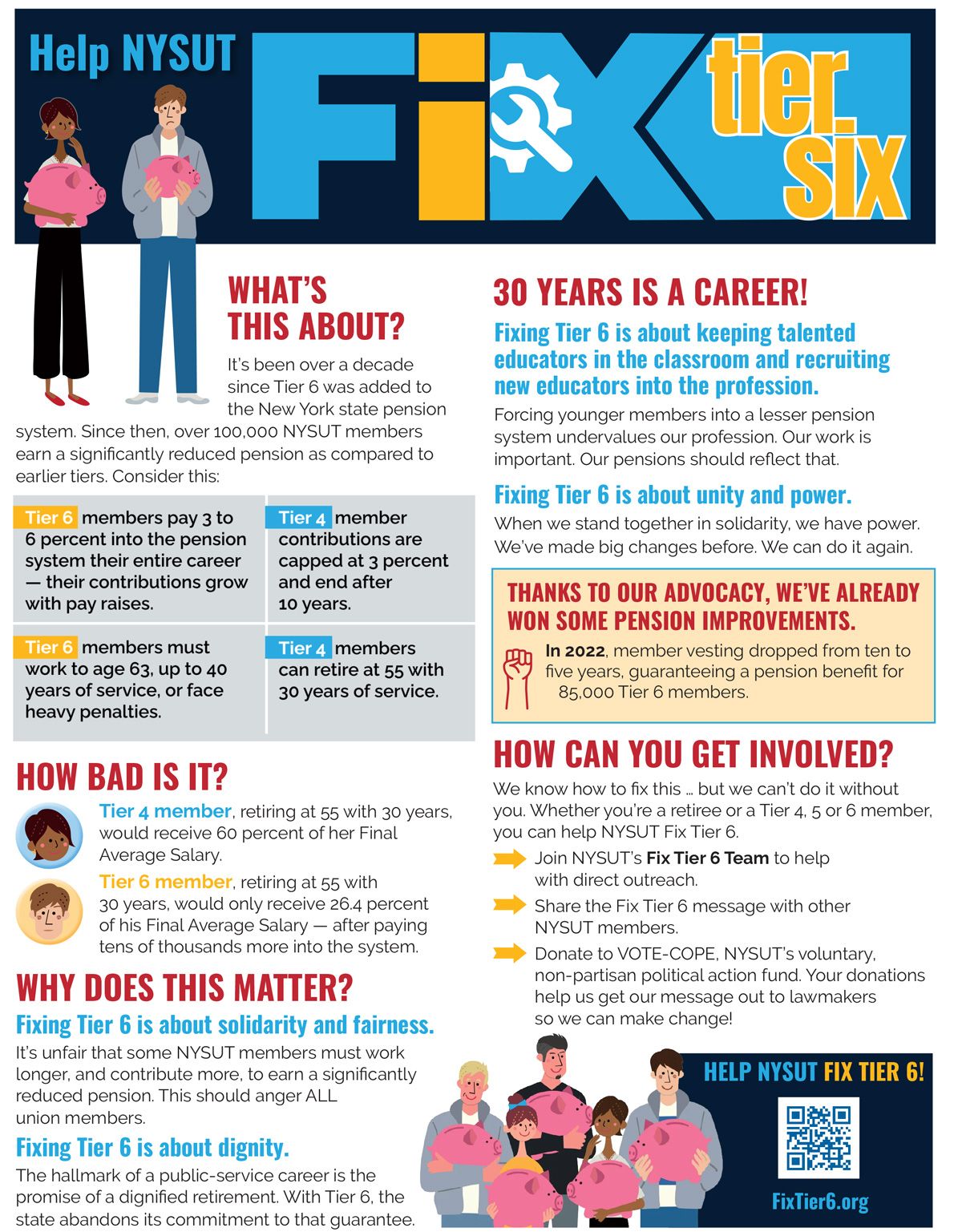

Source: fixtier6.org

Typical years of service required

Requirements vary widely, but common ranges and benchmarks include:

-

10 to 15 years

Many plans allow a reduced or partial pension at this point, or vesting (the right to a future pension) often occurs here. -

20 to 25 years

A frequent milestone where teachers can claim retirement with reasonable benefits. Some systems offer full benefits after 20–25 years. -

25 to 30+ years

Typical for full, unreduced pensions in many public systems. Higher final-pay growth and longer service produce a stronger payout. -

Age-based rules combined with service

Rules like “age 55 with 30 years” or “age + years = 80/90” are common. These let some teachers retire earlier if they have long service.

Examples of how many years to retire as a teacher depend on your plan’s vesting period and full-benefit criteria. If you want certainty, check your plan document or ask your retirement office for specific thresholds.

Source: ed100.org

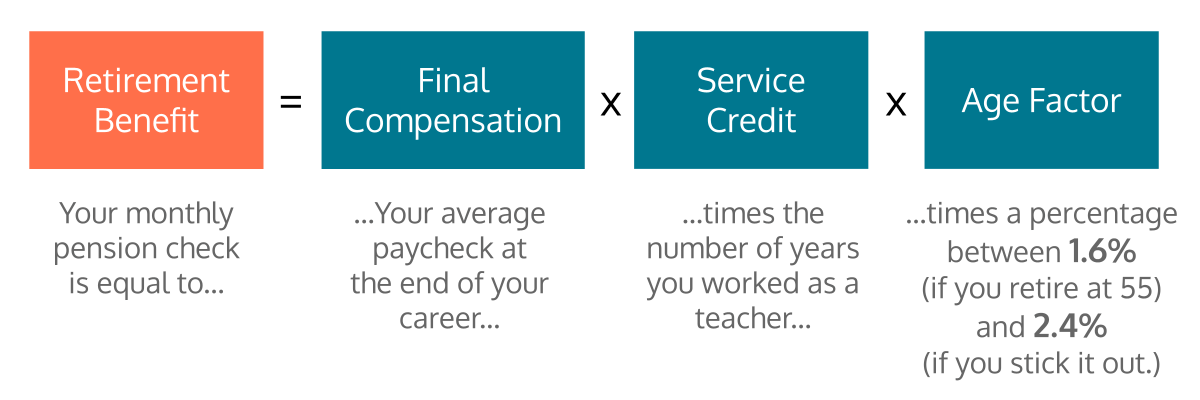

How teacher pensions are calculated (simple formulas and examples)

Most pension calculations use three parts: years of service, a multiplier, and a final average salary. A simple formula looks like this:

Pension = Years of service × Multiplier × Final average salary

Typical multiplier range: 1.5% to 2.5% per service year. Here’s an example:

- 30 years × 2.0% × $60,000 final average salary = 30 × 0.02 × 60,000 = $36,000 per year

If you retire earlier, the pension may be reduced. For example, retiring at age 55 instead of 60 might reduce the multiplier or apply an actuarial reduction like 5% per year early.

Understanding how many years to retire as a teacher means running projections with your own salary numbers and multipliers. Use conservative salary estimates and factor in cost-of-living adjustments when available.

Source: etsy.com

State, district, and plan variations to watch

Teacher retirement is not uniform. Key differences include:

-

Public state teachers

Most are in state or regional public pension systems with defined benefits and specific vesting rules. -

Teachers in Social Security systems

Some teachers also contribute to Social Security. That affects how many years to retire as a teacher because Social Security benefits add income and have separate age rules. -

Private and independent schools

Often they lack large pension plans. Teachers typically rely on 403(b), 401(k), or personal savings. -

Early-retirement incentive programs

Occasionally districts offer buyouts or incentives for early leave. These change the math for how many years to retire as a teacher.

Always ask your plan administrator for written details on vesting, eligibility age, multipliers, and survivor or disability options. Those specifics determine the true answer to how many years to retire as a teacher for your situation.

Source: amazon.com

Strategies to retire earlier or with better benefits

You can influence how many years to retire as a teacher by planning early and using smart moves:

-

Maximize service credit

Buy back eligible prior service, substitute teaching years, or military service when allowed by your plan. -

Time your final salary

Since pensions often use final average salary, plan promotions or peak pay years strategically. -

Contribute to supplemental accounts

A 403(b), 457(b), or IRA can bridge gaps if your pension is small or you face early retirement penalties. -

Coordinate Social Security and pensions

If you’re covered by both, plan Social Security claiming to optimize lifetime income. -

Consider phased retirement options

Some employers allow part-time work or phased retirement to reduce benefit reductions.

From my experience advising teachers, buying limited eligible prior service once saved a colleague several thousand dollars in lifetime pension value. Small proactive steps add up.

Source: wzzm13.com

Financial planning: income needs and replacement rates

Aim to replace a portion of your working income in retirement. Many planners suggest 70%–80% replacement from all sources combined. Steps to estimate:

- Add expected pension income, Social Security, and retirement account withdrawals.

- Subtract expected expenses you’ll no longer have, like commuting.

- Test scenarios where you retire after 20, 25, and 30 years to see differences.

If your pension is small after 20 years, you may need larger personal savings. Understanding how many years to retire as a teacher connects directly to how comfortable your retirement will be.

Source: toledoblade.com

Common pitfalls and limitations

Be aware of these traps when planning years to retire as a teacher:

-

Assuming all systems are the same

Different rules can change eligibility and benefit size. Verify your plan. -

Ignoring inflation and healthcare costs

Pensions may not keep pace with rising healthcare or living expenses. -

Overlooking survivor and disability provisions

Failing to plan for dependents can leave loved ones exposed. -

Not accounting for early-retirement penalties

Retiring too early can permanently reduce lifetime income.

I once saw a teacher retire after 18 years thinking benefits would be near-full. The realized benefit was heavily reduced. Always get a benefit estimate before deciding.

Source: waterfordschool.org

Two quick PAA-style questions

What counts as years of service for teacher retirement?

Years usually include full-time teaching in the system, approved leaves, and sometimes substitute service if the plan allows. Purchased prior service or military time can add to total years.

Can you collect a pension and work part-time?

Many plans allow part-time work after retirement, but rules vary on reemployment limits and how that affects pension payments.

Frequently Asked Questions of how many years to retire as a teacher

How many years do you need to vest in a teacher pension?

Vesting commonly takes 5 to 10 years in many plans. Once vested, you have a right to a future pension even if you leave before full retirement.

At what age can a teacher retire with full benefits?

Full-benefit ages vary but often fall between 55 and 65, sometimes tied to years of service. Age rules differ by plan and can include combined age-plus-service formulas.

Can I retire after 20 years as a teacher?

Yes, some plans allow retirement after 20 years with reduced or even full benefits depending on age and plan rules. Check your specific plan’s early-retirement terms.

Will Social Security change how many years to retire as a teacher?

If you participate in Social Security, it supplements your pension and affects how you time retirement. Some teachers are exempt from Social Security, which changes planning needs.

Is it possible to buy back service to retire earlier?

Many systems let you buy back eligible prior service, which can shorten the time needed to retire or increase your final pension amount.

Conclusion

Knowing how many years to retire as a teacher starts with reading your plan documents, running simple pension projections, and planning for gaps with savings. Aim to understand service credit, vesting, multipliers, and age rules so you can pick the right retirement year. Take action now: request a formal benefit estimate, review buyback options, and set up or increase supplemental retirement savings. If you found this helpful, leave a comment or subscribe for more teacher retirement guides and tools.

Retirement Planning Writer & Financial Lifestyle Expert

Michael Reynolds is a senior contributor at RetirementGazette.com, where he focuses on helping readers navigate the journey toward a secure and fulfilling retirement. With over a decade of experience in personal finance, retirement planning, and lifestyle writing, Michael combines practical strategies with easy-to-understand guidance tailored for both pre-retirees and those already enjoying their golden years.

His work covers a wide range of topics including retirement income strategies, smart investing, post-retirement careers, and everyday financial decisions that shape long-term stability. Michael believes that retirement is not just about saving money—it’s about creating a balanced life with purpose, flexibility, and peace of mind. This perspective aligns with modern retirement thinking, where financial planning and lifestyle choices go hand in hand.

At RetirementGazette.com, Michael is committed to delivering well-researched, unbiased, and actionable content. He carefully analyzes financial trends, expert insights, and real-world scenarios to help readers make confident decisions about their future. His mission is simple: to empower individuals with the knowledge they need to retire smarter, live better, and enjoy every stage of life after work.